The Theory of Bounty Tournaments – Part 2: ICM and Equity Drops

In part 1 of “Introduction to Bounty Theory,” we analyzed how the structures of bounty tournament prize pools form the basis for several potentially significant insights into the fundamental differences between bounty and non-bounty MTTs. In particular, we noted that the two prize pools—the bounty prize pool and the regular prize pool—have different natures:

- The regular prize pool functions the same as in regular, non-bounty tournaments and can be modeled by ICM.

- The bounty prize pool, however, is not distributed by placement in the tournament and so can not be modeled by ICM but largely follows the Chip EV model instead.

Building on the foundation of these observations, this article takes a deeper dive into the theoretical implications of understanding the two prize pools as operating distinctly but in concert together throughout a bounty MTT.

In particular, this article will explore how and why:

- The impact of ICM on the regular prize pool competes with the $value (equity drop) of winning the bounty instantly and increasing our proportional (Chip EV) share of the bounty prize pool as a bounty MTT progresses.

- The optimal strategies for winning the most from the total prize pool may differ significantly from classic tournaments because of the ways that winning a bounty impacts the potential total $value of our stack if we win an all-in pot as the covering player.

ICM and Bounty Equity Drops

At any point in a bounty MTT, players simultaneously experience a positive (ICM) risk premium in relation to the regular prize pool and a negative (bounty) equity drop—for covering players only—in relation to the bounty prize pool. Both covering and covered players also have their bubble factors impacted by their future Chip EV share of the bounty prize pool (see the bounty bubble factor formula below).

Equity drop refers to the negative risk premium pressure that the value of the bounty adds to our calculation of the bubble factor (BF)—or total risk premium—for a given spot.

Let’s consider ICM bubble factors for each format:

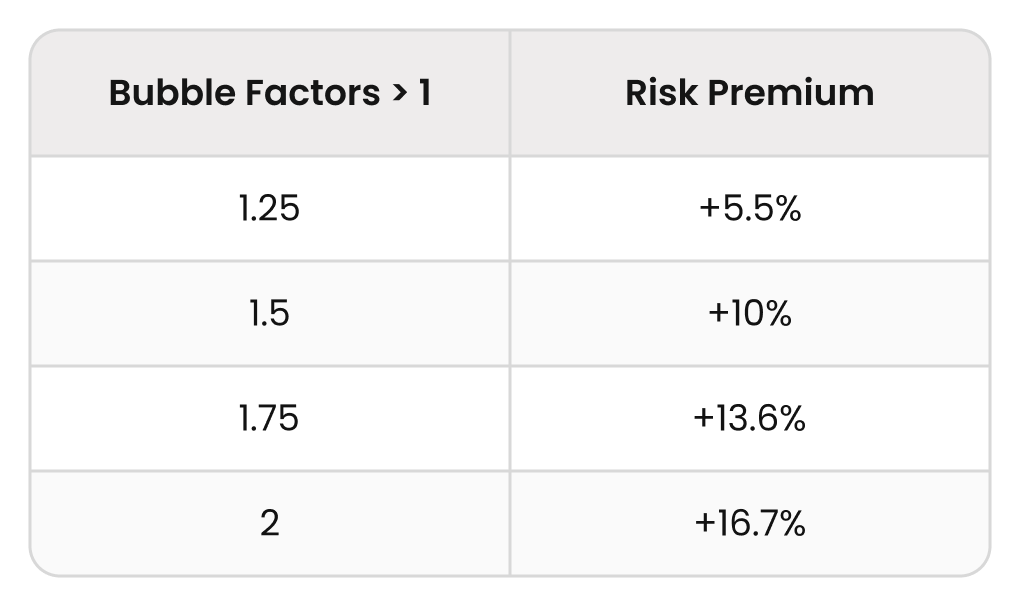

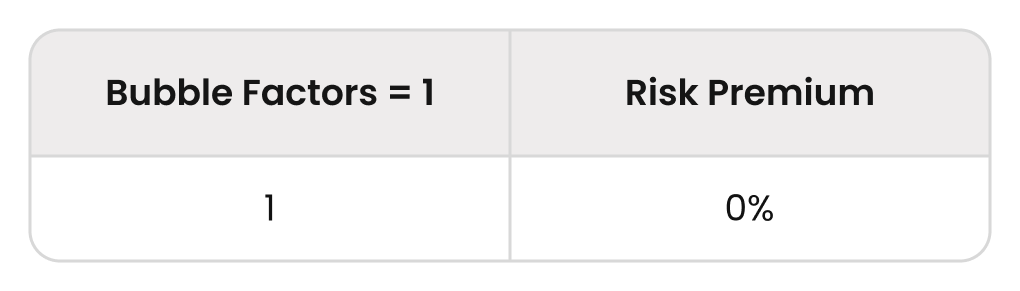

- In regular, non-bounty tournaments, bubble factors are always >1 and thus correlate to positive risk premiums (expressed in percentages). For example, a bubble factor of 1.5 converts to a +10% risk premium.

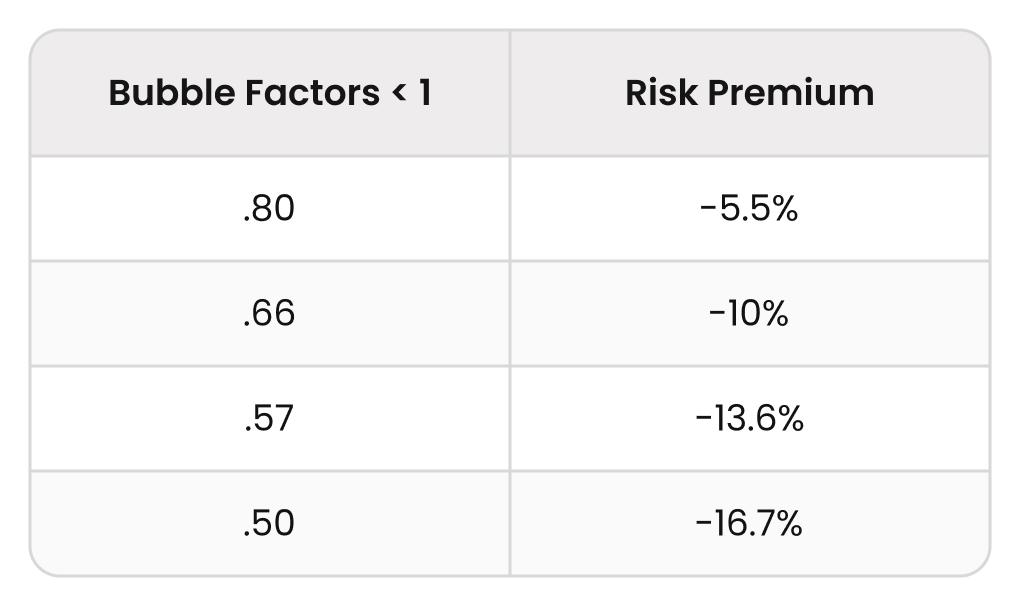

- In bounty tournaments, however, bubble factors can be <1, which convert to negative risk premiums.

(A bubble factor of 1 = zero risk premium or Chip EV.)

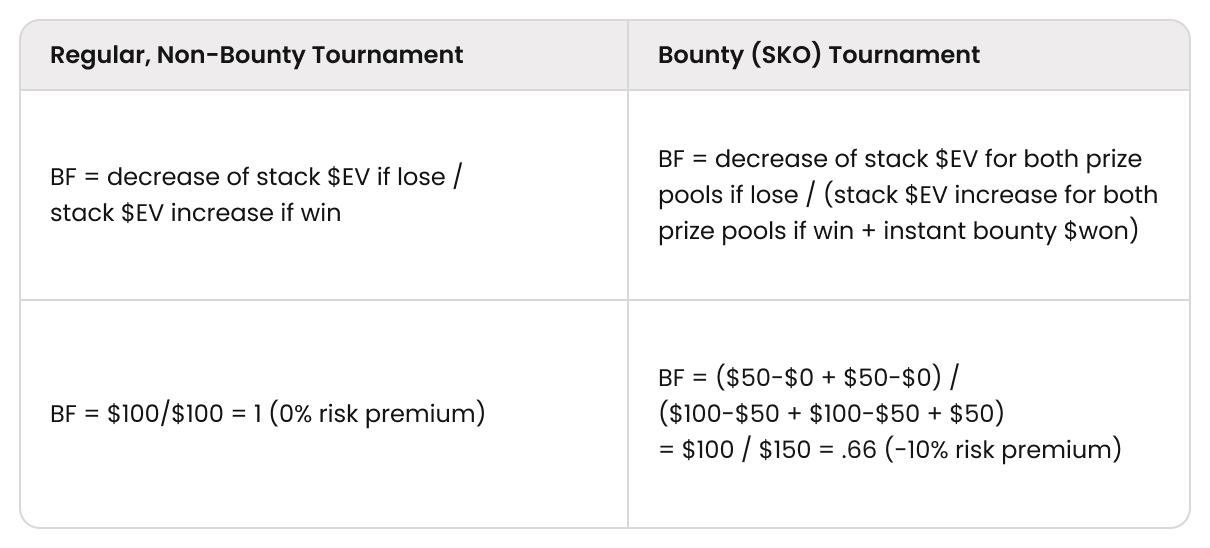

This is because, when a bounty is in play, we add the $value of the instant bounty to be won to the value of our stack if we win the (all-in) pot, as well as the future EV of winning bounties later in the tournament. The below toy game example provides a demonstration of the fundamental variables that impact the calculation of bubble factors in all types of MTTs. In this theoretical example, we assume SB shoves all-in, and BB calls the first hand of a $100 regular tournament and a $50+$50 Standard Knockout (SKO) bounty tournament (no antes):

In a regular tournament, doubling up the first hand roughly doubles our stack $EV (this is rounded up; in reality, it will be slightly less than 2x because some of the tournament equity from busting a player will be distributed to all the other remaining players). Similarly, in an SKO tournament, our stack $EV for the regular prize pool also (slightly less than) doubles if we win an all-in pot in the first hand. In addition, in the SKO, our share of the bounty prize pool almost exactly doubles because the bounty prize pool is modeled by Chip EV—plus, we also immediately win $50.

The bubble factor in the regular tournament can never be <1 because the potential increase in our stack $EV when winning a pot can never be greater than the decrease in our stack $EV if we lose. The fundamental principle of ICM is that the chips we win are worth less than the chips we lose. In the early stages of the tournament, this difference is subtle and negligible, but it becomes clear in stages of the tournament that are highly pressured, such as money bubble and final table spots.

Final Table Example: ICM and Equity Drops

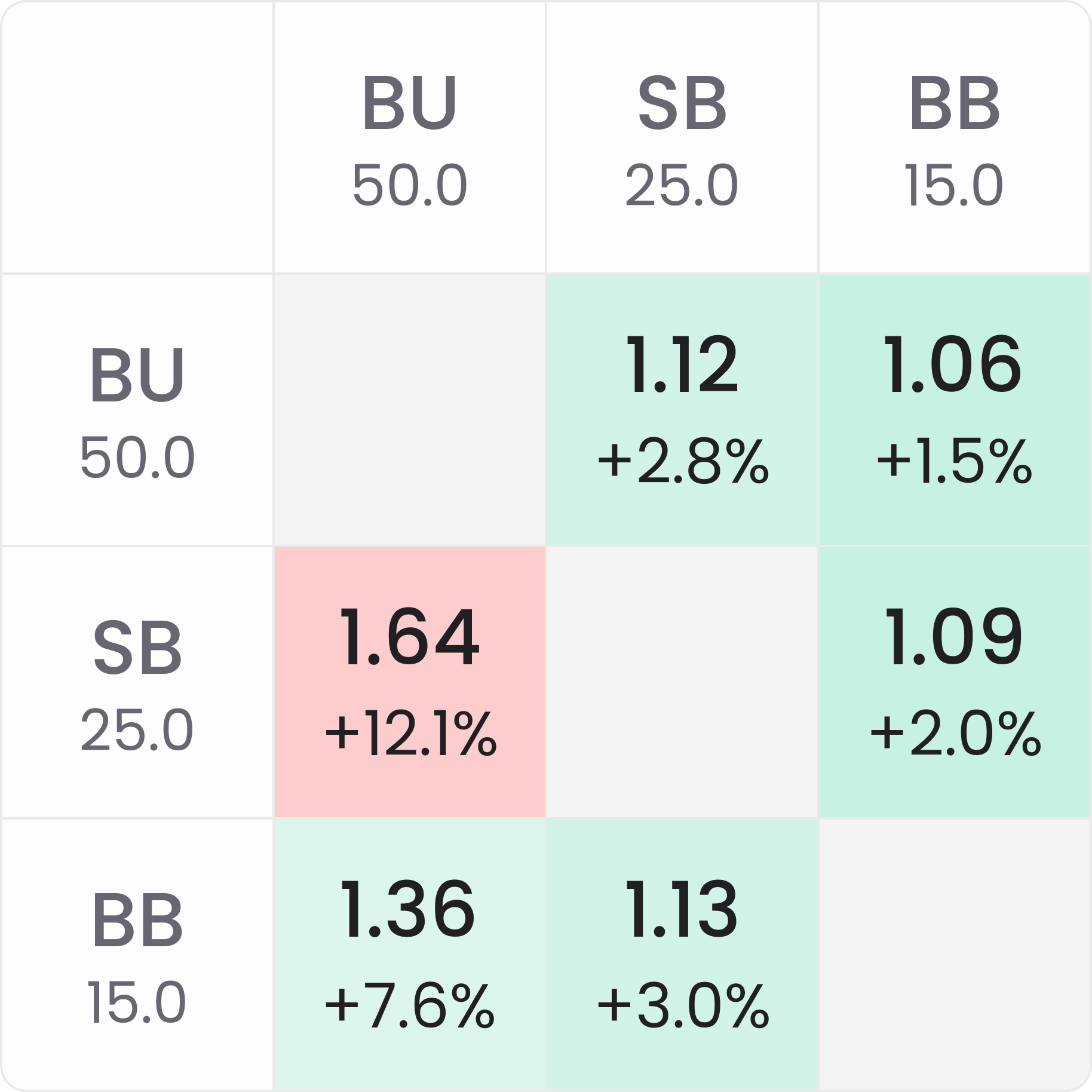

Below, we compare the bubble factors and how they are calculated in two different tournament formats with three players remaining.

The regular, non-bounty $100 tournament

- The prize pool remaining = $700 with the following payouts:

- $400

- $200

- $100

The SKO $50+$50 tournament

- Same payouts for the regular prize pool

- The bounty prize pool remaining = $150 ($50 bounty per elimination of each of the three remaining players)

- The total prize pool remaining = $850.

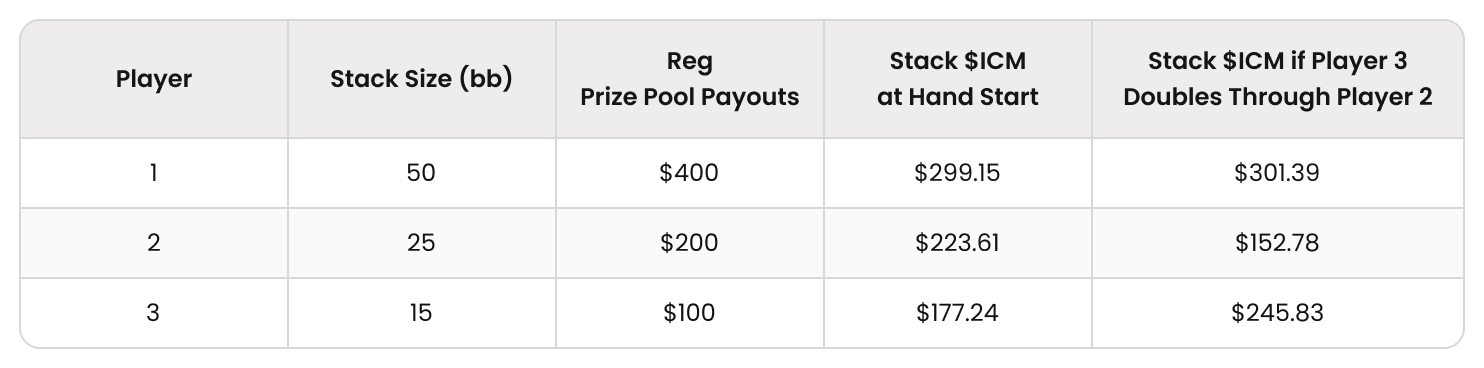

With three players remaining, the 15bb short stack has an $ICM value of ~$177 at the start of the hand ($ICM stack values here were solved by an ICM calculator). If the 15bb stack doubles through the 25bb stack, their 30bb stack will then be worth ~$246, but they will only win $100 if they lose an all-in confrontation. Thus, the 15bb short stack bubble factor vs. the 25bb middle stack is:

Regular MTT BF = decrease of stack $EV if lose / stack $EV increase if win

($177 – $100) / ($246 – $177) = $77 / $69 = 1.13 BF (approx. +3% RP)

And conversely, the 25bb middle stack bubble factor vs. the 15bb short stack is:

($223.61 – $152.78) / ($288.89 – $223.61) = $70.83 / $65.28 = 1.09 BF (+2% RP)

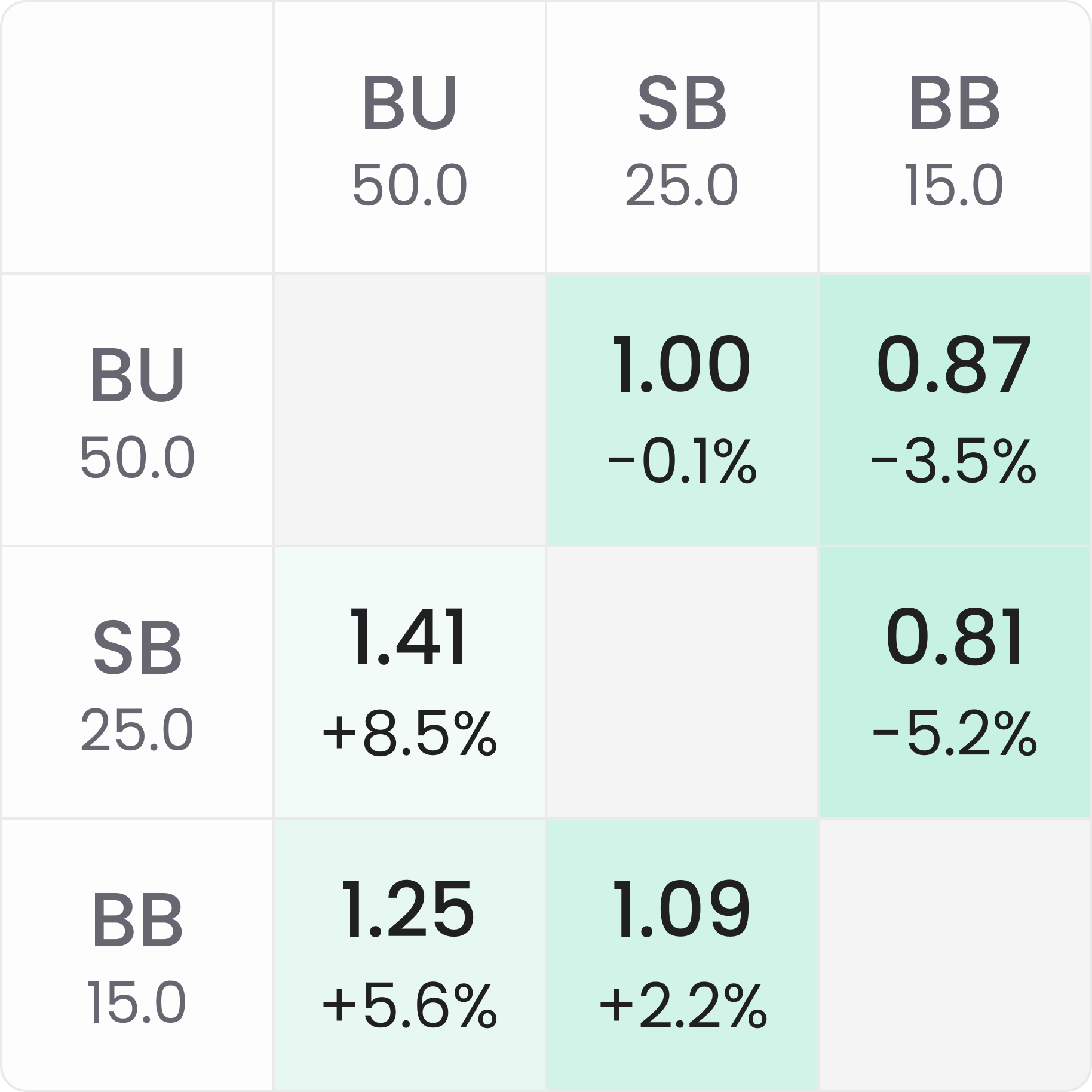

However, all of the bubble factors are lower if we change the above scenario to a $50-$50 SKO bounty tournament (with the same payouts for the regular prize pool), including for the covered players:

→

In the SKO, the middle stack’s share of the Regular Prize Pool (RPP), whether they win or lose the all-in confrontation, is the same as in the non-bounty tournament. For the bounty prize pool, if the 25bb stack busts the 15bb stack, they will win an extra $50 bounty instantly, and their share of the remaining $100 Bounty Prize Pool (BPP) will increase from $41.67 to $44.44. Each player’s share of the remaining bounty prize pool is calculated by the proportion of their stack size to the total chips in play (the “proportional” or Chip EV method). So, we can calculate the bubble factor of the 25bb middle stack vs. the 15bb short stack as:

Bounty MTT BF = ($223.61 – $152.78) + ($41.67 – $16.67) / ($288.89 – $224) + ($44.44 – $41.67) + $50

= $95.83 / $118.05 = .812 (-5.2% RP)

Now that we’ve calculated the bubble factor for the mid stack vs. the short stack, we can see that the equity drop is going to be approximately -7%+2% RP ICM – (-5%) RP Bounty.

The equity drop is the difference between the total risk premium without the bounty in play and the risk premium with the bounty in play.

Bubble Factors, Total Risk Premiums, and Bounty MTTs

Bubble factors in knockout tournaments are calculated differently than in regular MTTs because of the extra value of winning a bounty when we bust a player (whether in the current or future hands). Due to the extra payout mechanism, the bubble factors of all players are also lower than in non-bounty tournaments. Though a covered player cannot access any portion of the remaining bounty prize pool in a hand where they are the shorter stack, there is still less ICM pressure on the covered stack due to the fact that a smaller % of the total prize pool is impacted by ICM vs. 100% of the prize pool in regular tournaments. In addition, there is always the potential for a covered stack to increase their stack to get (more) access (see future bounty EV).

This “future bounty EV” is expressed in bounty bubble factor calculations as the decrease and increase in stack $EV for the bounty prize pool if the player loses or wins the pot. Because all players with chips have a share in the bounty prize pool, which is modeled by Chip EV and not impacted by ICM, there are lower bubble factors in bounty tournaments overall. In fact, a covered player’s share of the bounty prize pool will exactly double if their stack size doubles.

ICM Risk Premiums and Equity Drops Are Additive

We observed in the previous article that the prize pool in a bounty MTT is split into two parts. We can also see in the bounty bubble factor formula that the decrease and increase of a player’s share of each prize pool are calculated separately and added together in the numerator and denominator of the formula.

Thus, we can extrapolate that the bubble factor in a bounty MTT can be generally expressed as:

Total Risk Premium (Bubble Factor) = Regular Prize Pool (Positive) Risk Premium + Bounty Prize Pool (Negative) Equity Drop.

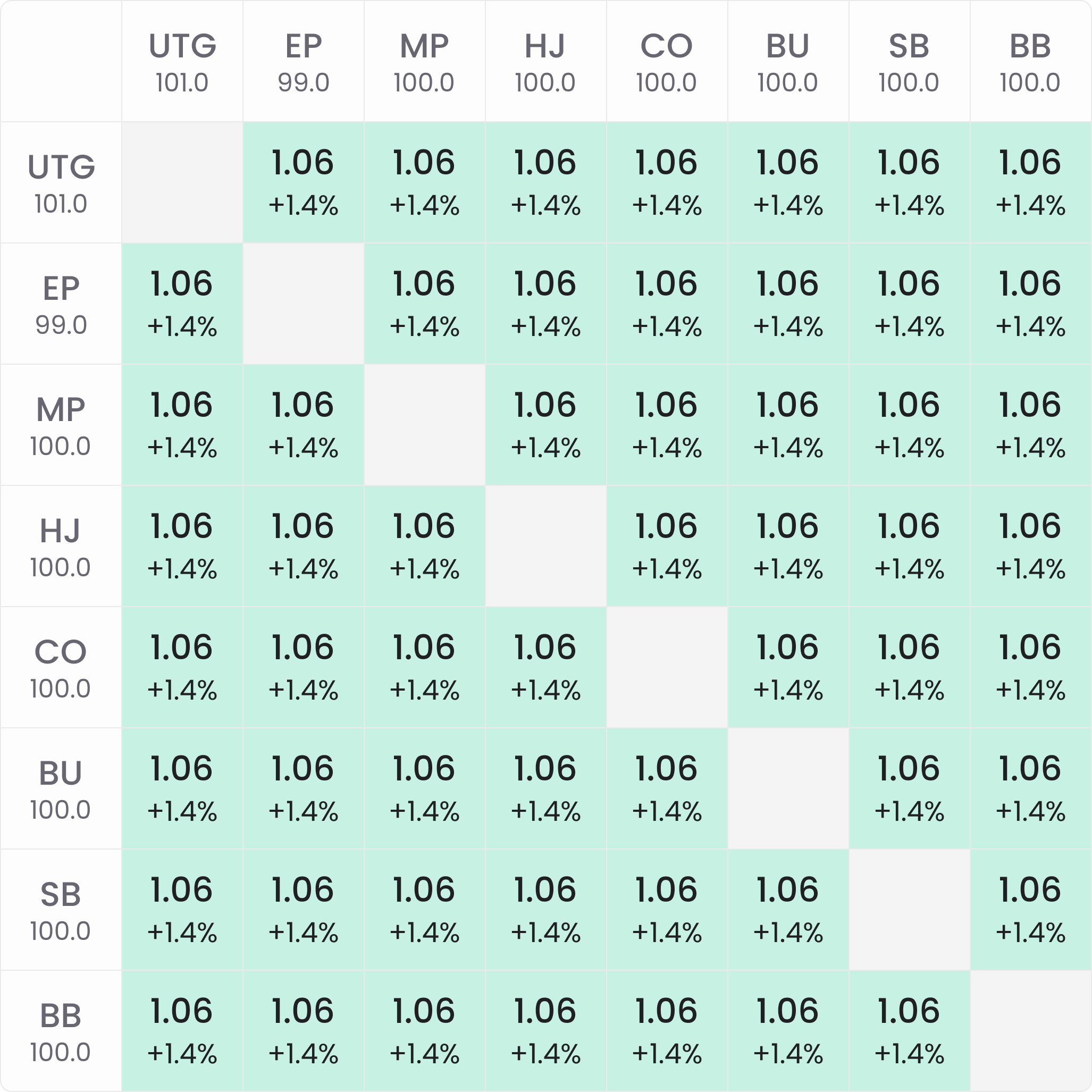

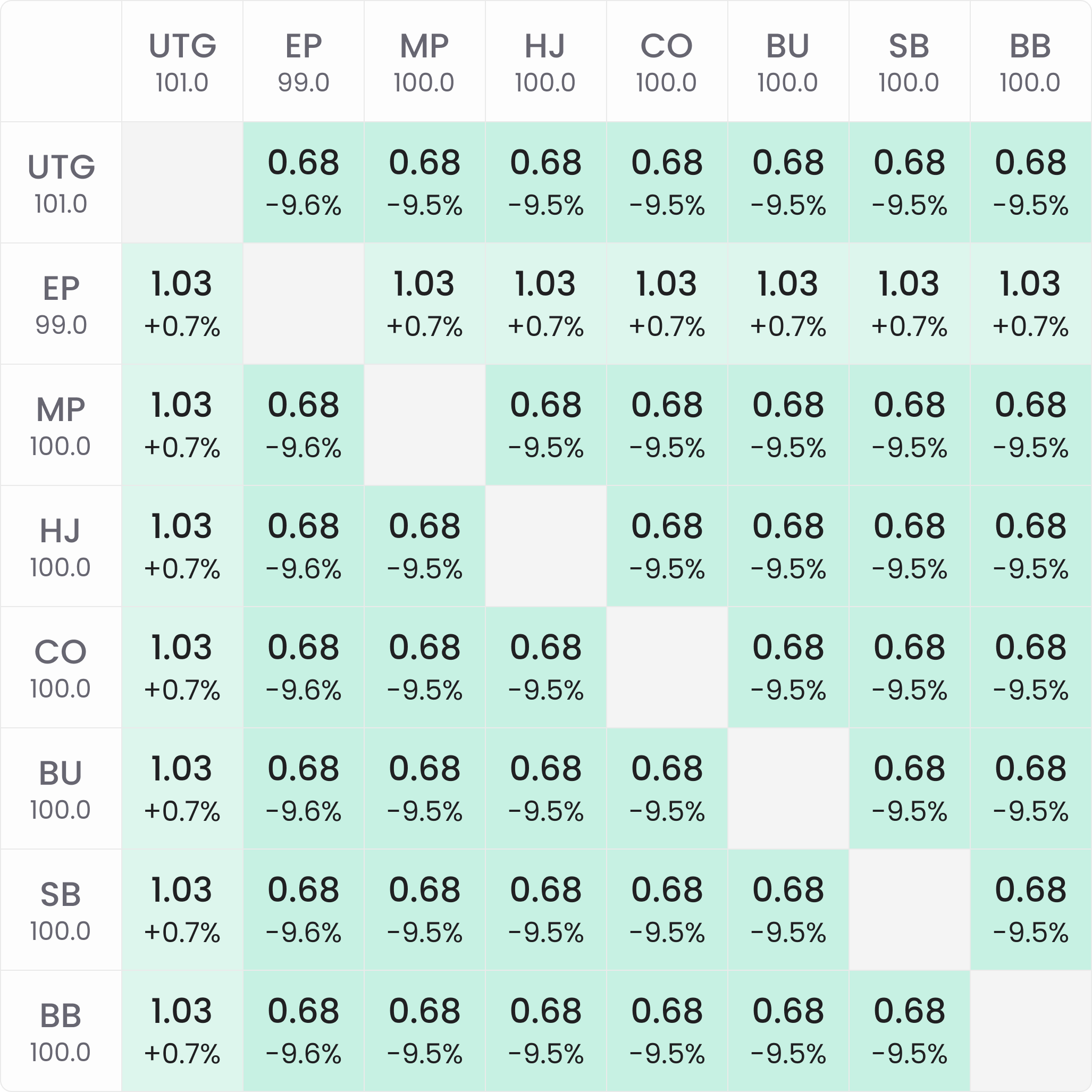

We can then use solvers to test this hypothesis. Below are the bubble factors at the start of two MTTs, both with a $100 buy-in and 1000 runners. On the left is a classic MTT, and on the right is an SKO ($50 bounty):

→

Looking at the above bubble factors, we can make the following observations:

- In the classic MTT chart, the total risk premium for each player is +1.4% at the start of the tournament.

- In the SKO chart, the total risk premium for the covered stacks is +0.7% at the start of the tournament.

- In the SKO chart, the bubble factor or total risk premium for covering stacks is -9.5% to -9.6%.

In the toy game ICM model calculation earlier in this article, we determined that the equity drop for a bounty at the start of a 50% SKO ($50+$50 buy-in) was -10% (.66 bubble factor). We can also calculate this risk premium using the pot odds equation. Assuming a 10,000 chip starting stack, our share of the bounty prize pool will be worth ½ of the starting stack in a 50% SKO, or 5,000 chips (and our share of the regular prize pool is also worth 5,000 chips, for a total of 10,000). If we are in the Big Blind on the first hand of the tournament and the SB shoves all-in,

The required % equity to call = amount to call / (amount to call + opponent’s stack + bounty chip value)

= 10,000 / (10,000 + 10,000 + 5000) = .4 or 40%

With the bounty EV expressed metaphorically in chips—since we don’t actually win 5,000 more chips, we win $50 cash—we need 40% equity to call. Without the added EV of the bounty, we would need 50%, so the bounty causes an equity drop of -10%.

However, looking at the SKO bubble factor chart above, the players with a covering stack show a bubble factor of .68 (-9.5%) instead of .66 (-10%). Why?

The equity drop at the start of every 50% SKO will be -10%. However, in tournaments, there is already ICM pressure on the first hand. The covered stacks in the SKO bubble factor chart show a +.7% risk premium.

Added together, .7% + (-10%) = -9.3%; close to the -9.5% in the bubble factor chart but not exact. Why?

The .2% difference in this case is accounted for by the fact that the covering stack also wins the blinds and antes in addition to the opponent’s stack when they win the pot. It is also common to see minor deviations in the risk premium conversions due to the bubble factors being rounded to 2 decimal points.

Conclusion

In bounty tournaments, the value of the bounty of a covered player—expressed either in terms of chips added to the pot or as an equity drop percentage—is static.

There are multiple ways to establish this as an axiom. Here are two of them:

- Via the pot odds calculation of the equity drop. At the start of the 50% SKO, the value of the bounty in chips is ½ of the starting stack, regardless of the covered player’s stack size.

- Via the demonstration that the positive and negative risk premium pressures associated with the regular and bounty prize pools are additive, as their sum equals the total risk premium that correlates with the bubble factor.

However, the positive risk premiums associated with the regular prize pool are very sensitive to stack sizes. Thus, even though the value of each covered player’s bounty is the same for all covering players, the bubble factors or total risk premiums of all of the covering stacks will differ depending on the stack distribution of all the players at the table and in the entire tournament because of how stack distribution heavily impacts the ICM pressure from the regular prize pool.

In the next (and concluding) article in this “Introduction to Bounty Theory” series, we will explore how to implement these theories about the prize pools in bounty tournaments to determine the value of the bounty in chips and equity drops for the start of the bounty period in SKOs and PKOs.

Wizards, you don’t want to miss out on ‘Daily Dose of GTO,’ it’s the most valuable freeroll of the year!

We Are Hiring

We are looking for remarkable individuals to join us in our quest to build the next-generation poker training ecosystem. If you are passionate, dedicated, and driven to excel, we want to hear from you. Join us in redefining how poker is being studied.

Latest article

The Case for the Hero Check: Why Great Players Know When Not to Bet

In this era of game theory and solvers and poker games running at a huge…

What’s Your Hand Worth? From Thin Value to Playing for Stacks

Poker theory offers many conceptual tools for answering the question, “What is your hand worth?”…

Tournament Poker’s Hidden Stakes

In this era of game theory and solvers and poker games running at a huge…

Top GTO Wizard Features the Pros Prioritize (and What They Leave Out)

In this roundtable series, I have been asking GTO Wizard content creators about some of…

How To Prep Like a Pro for WSOP

The World Series of Poker (WSOP) is one of the most recognized tournament series in…

Cold-Calling in Straddle + Ante Games

In traditional no-limit Hold‘em cash games, calling an open-raise is rarely appealing unless you are…

Roundtable: Aha! Moments in GTO Wizard

Understanding solver technology is very challenging. You not only have to grapple with the technology…

Poker: The Battle for Information

Poker is sometimes described as a battle for information, and there is much truth in…

How To Construct a Squeezing Range

As is often the case with my articles for this blog, what I am writing…

Opening From the Blinds in Straddle + Ante Games

Opening From the Blinds in Straddle + Ante Games No-limit Hold‘em has not traditionally been…

When To Just Shove Post Flop in ICM Spots

When To Just Shove Post Flop in ICM Spots The general trend for bet sizing,…

The Theory of Bounty Tournaments – Part 3: Key Calculations

Parts 1 and 2 in this bounty theory series describe how total risk premiums are…

The Learning System That Separates the Best From the Rest

As an avid strategy game enthusiast, I’ve spent a large portion of my life trying…

The Fish Were Right All Along

In a recent conversation with Andrew Brokos, he made the comment, “The fish were onto…

How to Use Practice Mode in GTO Wizard to Improve Your Game

GTO Wizard provides a wide variety of tools to help you become a better player,…

Should You Ever Bluff with a Pair?

Turning a made hand into a bluff might initially sound counterintuitive. In the pre-solver days,…

ICM Strategy: Playing IP Against the Chip Leader on the Final Table

The good news is you’ve made the final table (FT). Better yet, you’ve made it…

ICM Survival Guide: How To Play OOP vs. a Covering Stack at the Final Table

Contesting a pot against a player who covers you at a final table (FT) is…

We’re At The River. Our Hand Can’t Win. Now What?

You’re in a heads-up pot and you’ve made it to the river. Your opponent has…

When Is Bluffing Profitable? The Key Factors You Need to Know

When is bluffing profitable? When you expect your opponent to fold! That’s not a joke,…

Blockers & Unblockers: The Secret to Picking Great Bluffs

Blocker/unblocker was a concept my coach, Dara O’Kearney, showed me in relation to bluffs. It…

The Art of Game Selection for MTTs: Finding Soft Fields & Extra Value

Game selection is not something immediately associated with tournaments because the seat draw is random.…

How To Get the Most out of Your Hand Reviews

I don’t spend much of my study time checking whether specific hands I played are…

The Art of Turn Probing: Exploiting Checked Flops

After calling a 3-bet as the out of position (OOP) player, you should expect to…

How To Respond to Large Preflop Raises in Poker

Solver-derived preflop charts for both cash games and tournaments have historically assumed small raises on…

Mastering Postflop ICM: Avoid These Common Mistakes

The new postflop ICM feature from GTO Wizard is a game changer. Previous incarnations of…

What Happens When Playing Chip EV and ICM Is Significant

Just how costly is it to play a Chip EV style when ICM is significant?…

How To Become a Winning Poker Player in 2025 – Part 2

Welcome back to part 2 of our series on how to become a winning poker…

How To Become a Winning Poker Player in 2025 – Part 1

I fell in love with the game of poker when I saw the best players…

IP 4-Betting in Deep-Stacked Cash Games

4-betting in position (IP) is a totally different phenomenon from 4-betting out of position (OOP).…

OOP 4-Betting in Deep-Stacked Cash Games

4-bet pots (4BP) can be scary because the stakes are high, but with 100bb stacks,…

Fixing a Poker Leak Part 2: The Mental Game

In the first part of my series on fixing leaks, I looked at the many…

Fixing a Poker Leak Part 1: Spotting and Correcting Errors

In this two-part series, I am going to look at how we can identify and…

How Significant Is ICM During Late Registration?

One of the many valuable aspects of GTO Wizard’s new postflop ICM feature is that…

The Many Faces of Balance in Poker

When you think of balance in poker, what comes to mind? Most likely, you were…

Unwrapping GTO Wizard’s Hidden Gems for 2025

A new year is upon us, which is classically the time that most people start…

The Theory of Bounty Tournaments – Part 2: ICM and Equity Drops

In part 1 of “Introduction to Bounty Theory,” we analyzed how the structures of bounty…

The Theory of Bounty Tournaments – Part 1: Prize Pool Fundamentals

Bounties are a significant new variable to take into account when studying tournament theory and…

Responding to Donk-Bets at Final Tables

It’s scary to contest a pot against a covering stack when you have a high…

Donk-Betting As the Covering Stack in MTTs

Tournament poker generally incentivizes stack preservation and more conservative play than cash game poker, and…

Dominate the River in 3-Bet Pots OOP

Playing the river may seem scary. Pots, on average, have been swelling up big time…

Exploiting BBs Who Never Donk-Bet

In a single-raised pot (SRP), a BB caller should almost always check when out of…

Picking the Right Semi-Bluffs

As I often like to remind readers, I am not a professional poker player; I…

Playing Calls From the Button in Cash Games

When first beginning to study cash game poker strategy, there is a common refrain that…

Bringing It All Together: PKO Review

Throughout the past year, our writers have presented nine unique articles and videos outlining how…

What Factors Impact Ranges the Most in PKOs?

In our article “How Does ICM Impact PKO Strategy?“, we contrasted how PKO and Classic…

PKO vs Classic: Postflop Play

In our previous articles comparing PKO and Classic tournaments, we reviewed how to adapt our…

How Do Bounties Impact Our Flop Ranges When Covering?

The previous articles in our PKO series showed how preflop ranges that are adjusted for…

Short Stack Stealing on the Bubble

Open-raising on the bubble into players who cover you is scary. Savvy opponents will recognize…

Maximizing Monsters in Deep-Stacked Scenarios

Why did Dracula quit the game when Wolfman insisted on a mandatory straddle? — Why?…

Confronting Monsters Under the Bed in Poker

Do you hide from things that go bump in the night? Does the sight of…

Bullying the Blinds With Continuation Bets

A big stack in No Limit Hold‘em does not always carry a license to steal.…

A Comprehensive Guide to Playing Satelites

One of the most important inventions in poker that contributed to the growth of the…

A Comprehensive Guide to Playing Mystery Bounties

The Mystery Bounty format looked like a novelty event at first, but swiftly became a…

Leading Hands That Should Check-Call

The most consistent leak I have encountered live and online, and at a variety of…

Mastering Turn Play in 3-Bet Pots OOP

Playing the flop OOP in a 3-bet pot can be challenging. Turn play, however, is…

PKO Versus Classic: Responding to 3-Bets

One of the keys to adapting to new game formats, such as Progressive Knockout (PKO)…

PKO Versus Classic: Responding to a Preflop Open

One of the keys to adapting to new game formats, such as Progressive Knockout (PKO)…

Preflop Range Morphology

Morphology in poker is the study of shapes/forms of ranges. This domain of poker study…

The Five Imbalances of Exploitative Poker

One of the great modern debates in poker is GTO vs Exploitative strategy. It can…

PKO Versus Classic: Preflop RFI Range Comparisons

One of the keys to adapting to new game formats, such as Progressive Knockout (PKO)…

Why So Much? An Exploration of Larger-Than-Geometric Bet Sizing

Via toy games, it is easy to demonstrate that a player betting a perfectly polarized…

Slow-Playing

Slow-playing, like running a big bluff or making a heroic call, feels great when it…

MDF vs ICM: Rethinking Bluffing & Defense Strategies in MTTs

Minimum Defense Frequency (MDF) is, strictly speaking, the calling (and/or raising) frequency that makes your…

The Magic of Equity Buckets

One of the most daunting aspects of learning the modern game of poker, especially with…

Preflop Strategy in Straddled Pots

Many games allow “straddles,” where a player who is not in the blinds voluntarily posts…

The 5 Levels of Trainer Mastery for MTTs

Studying poker can be a challenge to both new and seasoned players. Tournament poker, in…

4-Bet Pots OOP as the Preflop Caller

4-bet pots are often uncomfortable to play. Some of the reasons include: — A lot…

Bounty Models Explained: Solving Knockout Tournaments

We’ve just rolled out a revolutionary update! You can now find optimal postflop ICM strategies…

Theoretical Breakthroughs in ICM

Today, we’ll share one of the most significant theoretical breakthroughs in tournament poker since the…

The Limitations of Nash Equilibrium in ICM Spots

In the complex world of poker tournaments, the Independent Chip Model (ICM) plays a pivotal…

Rake & Rakeback Explained: Optimize Your Poker Earnings

Rake is one of the main things that allows poker to distinguish itself as a…

From Gutshots to Airballs: Choosing Your Bluffs

Whenever you’re running a bluff, it’s reassuring to have a backup plan like some draw…

Crush 3-Bet Pots OOP in Cash Games

Did you know that 3-bet pots out of position (OOP) as the preflop aggressor make…

The Math of Multi-Street Bluffs

Bluffing is a fundamental skill in poker, blending deception with strategic calculation to sway the…

The Mechanics of C-Bet Sizing

What factors influence c-bet sizing on the flop? Is it fold equity, SPR, draw equity,…

Poker Insurance: Reducing Variance or Wasting Money?

Variance is what makes poker great. Without it, recreational players would not keep playing. Most…

Money Bubble vs Final Table Bubble

Is one bubble the same as another? Should we play more conservatively on the money…

Facing 3-Bets From Covering Stacks at the Final Table

The last thing you want when you have a nice stack at the final table…

Poker Staking Essentials

One of the great ‘through the looking glass’ moments for any poker player is when…

That Harm Your Poker Study")

A Poker Player’s Guide to Conquering Cognitive Biases – Part 2

In the past, I’ve written about gambling biases that can affect how you play and…

The 5 Levels of Trainer Mastery for Cash Games

We’ve created over 40 custom drills for this article! Though all drills are accessible through…

How To Review ICM Preflop Ranges

In a sense, tournaments could be considered the more complex format compared to cash games.…

Calling Down Over-Bluffed Lines in Lower Limits

If you are playing low stakes, chances are you have a plummeting red line in…

A Poker Player’s Guide to Conquering Cognitive Biases – Part 1

In my article on confirmation bias, I mentioned that there are many cognitive biases and…

Exploiting Cold Callers Who Stab Too Much

In single-raised pots (SRPs) between an in position (IP) raiser and an out of position…

Using the 80/20 Rule in Poker

The Pareto principle, or the ‘80/20 Rule’, is an economic theory that, when you learn…

Attacking Aggressive Opponents When They Check Back Flop

Playing out of position (OOP) is hard. Playing out of position against an aggressive opponent…

Buying the Showdown

This article was inspired by Mark, who submitted a question to my podcast about a…

Barreling as IP Cold-Caller

You cold-called a preflop raise. That’s scary. You bet into a check from the preflop…

How Confirmation Bias Impacts Poker Study

There are a great number of cognitive biases, mental models, and heuristics that I plan…

A Champion’s Guide to Knockout Poker Formats

If you’ve opened any online poker client recently you will have seen an explosion of…

Pushing Equity With Small Bets

One of the most memorable pieces of poker wisdom I ever received came from my…

Turn Check-Raise Heuristics

Dealing with turn aggression is an area many players find difficult, which is an excellent…

Aggregate Flop Strategy: SB C-Betting in SRP

Continuation betting from the SB does not follow the usual patterns for out of position…

The Power of the Hypergeometric Bet

What size should we bet with our value and bluffs? When our range is perfectly…

The Limits of Nodelocking

GTO Wizard’s nodelocking feature is where the theory meets the practical; you can study how…

Limp-Called Pot as BB

My favorite way to study with GTO Wizard is to approach it experimentally, using the…

Why Not Shove?

You’re in the money in an MTT but still a long way from the final…

What We Can Learn From Outlier Hands

The worst way to use a tool like GTO Wizard is to simply ‘line-check’ how…

Building Exploits From Showdown

Understanding how and when to exploit opponents at a live poker table is a delicate…

Navigating Nasty Rivers Out of Position

Playing out of position (OOP) is hard. It’s fundamentally disadvantageous to act on each street…

Crack the Shell of Nut Draw Strategy

Nut draws hold obvious appeal as betting and raising candidates. They benefit from fold equity,…

Preflop Raise Sizing: Examining 2 Key Factors

It amazes me that, after nearly twenty years of playing no-limit hold ‘em professionally, I…

How to Handle Loose-Passive Limpers

Solver charts and presolved solutions do not offer much in the way of explicit guidance…

Top 5 Mistakes in Spin & Gos

As a Spin and Go poker coach, I regularly encounter common mistakes that players make,…

An Introduction to Spin & Gos

I was playing Tournaments for the first decade of my career. But after my first…

Relationships and Poker

In my more than 15 years of poker coaching, I’ve helped hundreds of clients improve…

Do Multiple Sizes Matter?

Should I work out the other tools or just stick to the crowbar? Solver results…

The Science of Learning Applied to GTO Wizard

The way we were taught to study in schools was flawed and has negatively impacted…

Check-Raising a Single Pair

In this article, I will address a question raised by Twitter/X user ’Matt Riley’, who…

The Turn Probe Bet

Imagine yourself defending as the BB caller vs BTN preflop raiser in a 100bb cash…

When To Encourage Multiway Pots in PKOs

I was recently shown this fascinating PKO hand from the GTO Wizard PKO library. Somebody…

Protect Equity and Prosper

When we think about the best hands to bet in a given situation, we tend…

Do Solvers Have Targets?

Targeting has long been a staple of exploitative poker thinking. When you’re value betting against…

Disciplining Big Blind in Limped Pots

When the BTN open-limps off a short stack, the postflop play against the BB should…

I’d Rather Be Drawing

Which is the better hand on a K♥8♦5♦ flop: K♠T♣ or 7♥6♥? OK, I’ll admit…

The Curious Case of Open-Limping Buttons

Before the advent of solvers, open-limping was considered the province of passive, gambley recreational players…

Cleaning Out Sticky IP Callers

A “sticky” player on your left, one who calls your preflop raises too often and…

Defending Against Tiny 3-Bets

Tournament poker is about precision. Cash games, where stacks typically run into the hundreds of…

Heads up! Exploiting SB’s Preflop Mistakes

Heads up (HU) tournament play presents unique challenges to the average player. Many tournament players,…

C-Betting As the OOP Preflop Raiser

Position is an extremely valuable advantage in poker. Most players would describe the comfort zone…

Overchoice: Making Sense of Multiple Sizings

Solver solutions with multiple bet sizes often involve a lot of mixing between those sizes,…

River Refinements: When Your Opponent Won’t Check-Raise

One of the biggest strategic differences between playing in versus out of position involves betting…

Turn Barreling in 3-Bet Pots

There are two articles on the GTO Wizard blog that make good prerequisites to this…

The Right Way To Think About Protection

Suppose Paul the Protector is in a 200bb cash game and opens A♠A♣ in the…

The Importance of Board Coverage

The first public version of the GTO Wizard announced AI upgrade already has some useful…

How To Adjust When Villain Has No Bluffs

“They always have it!” is a common, semi-joking expression in poker to describe the tendency…

Adjusting on Later Streets After Exploiting Flop

The key to exploiting opponents profitably is knowing when to stop. I’m not referring to…

C-Betting IP vs Passive Poker Players

A preflop raiser enjoys a significant range advantage over a BB caller, enabling them to…

C-Betting Against ICM Preflop Ranges

You raise from early position (EP) in a multi-table tournament and the BB calls. Both…

The Art of Bluff Catching

Bluff catching—calling a bet with a modest hand which you expect to win only if…

Exploiting Excessive C-Betting by IP

On some flops, it is simply not possible for the preflop raiser to continuation bet…

Is Limping Pimping?

In a past Discord post, one of our members noted that an upside of implementing…

Exploiting Excessive C-Betting by OOP

A preflop raiser who continuation bets too often is always a potential target for exploitation,…

Preflop Button Mastery in PKOs

Playing from the Button presents many unique opportunities in any tournament format, especially in PKOs.…

The Worst Turn Card

Greetings from GTO land. In today’s article, we will use the Turn Reports feature to…

Navigating Range Disadvantage as the 3-Bettor

Picture this: We’re playing a NL500 6-max cash game, and we’ve won a few pots,…

Mastering Three-Bet Pots In Position in MTTs

Playing in position against a three-better is a lesson in playing to your advantages. As…

Mastering Three-Bet Pots Out of Position in MTTs

Three-bet pots are scary. Playing out of position is scary. Put them together, and you’ve…

The Greatest Final Table in Triton History

Today, we’ll examine one of the most epic final table battles I’ve ever witnessed! Our…

Mastering Thin Value Bets in Checked-Down Pots

Valuing your hand appropriately—determining whether it’s strong enough to value bet or so weak you…

Maximizing Value on Monotone Flops

Monotone flops tend to provoke great anxiety among poker players. It’s easy to imagine that…

How to Defend Against Turn Donk Bets

Responding effectively to donk bets on the turn is tricky;, there’s no getting around that.…

How and Why You Should Use Turn Donk Bets

Donk betting–taking the betting lead away from the previous street’s aggressor–on the flop is rarely…

How Stack Sizes Change Your Range

In this series, we have looked at factors that can influence ranges in otherwise identical…

How to Leverage GTO Wizard’s EV Comparison Tool

With the advent of solvers, some troubling new turns of phrase have entered the poker…

Should You Ever Cold Call a 3-Bet?

When there’s been a raise and re-raise before the action is on you, you will…

When ICM Breaks Down

If you have read my previous GTO Wizard articles and my books, you’ll know I…

When Is It Correct To Fold AA Preflop?

One of the criticisms of ICM is that it is boring and robotic. In my…

OOP C-betting vs Loose Cold-callers

In a previous GTO Wizard article, I asserted that “Playing against an in-position cold-caller is…

Short-Stacked Play in MTTs

Playing a short stack well is an essential tournament skill. It is extremely rare to…

When To Ladder in Tournaments

In my last two articles, I wrote about the effect field size and payout structure…

How Payout Structures Impact ICM

Last time we discussed the ICM considerations in game selection, we looked at field size,…

C-Betting IP in 3-Bet Pots

When you three-bet before the flop and the original raiser calls from out of position,…

C-Betting OOP in 3-Bet Pots

Continuation betting from out of position can be a dicey proposition in single-raised pots. Cold…

Dynamic Sizing: A GTO Breakthrough

Dynamic Sizing is a revolutionary new poker algorithm that automatically simplifies your strategy with the…

Dynamic Sizing Benchmarks

Dynamic Sizing is a revolutionary new poker algorithm that automatically simplifies your strategy with the…

Understanding The Impact Of Field Size On ICM In Poker

When people talk about game selection in multi-table tournaments (MTTs), they invariably talk about the…

Defending vs BB Check-Raise on Paired Flops

This is a companion piece to Attacking Paired Flops from the BB; you will get…

Mastering PKO Final Tables

Final tables can be the most exciting and rewarding phase of a tournament, and being…

Attacking Paired Flops From the BB

Paired flops present unique challenges to both a preflop raiser and a BB caller. The…

KK vs QQ vs JJ at WSOP Main Event

With only fourteen players remaining in the 2023 WSOP Main Event and blinds of 400K/800K/800K,…

Responding to BB Squeezes

You open raise, someone calls, and the BB squeezes. How should you construct your strategy?…

Crushing a Top HUNL Poker Bot

In 2022, Philippe Beardsell and Marc-Antoine Provost, a team of Canadian programmers from Quebec, developed…

GTO Wizard AI Explained

We are excited to introduce GTO Wizard AI, formerly known as Ruse, the world’s best…

GTO Wizard AI Benchmarks

GTO Wizard has combined the power of artificial intelligence with traditional solving methods to bring…

Table Management in PKOs

Perhaps the most important strategic consideration in Progressive Knockout Tournaments (PKOs) is making sure you…

Overcalling From the BB

In poker, overcalling refers to calling a bet or raise after another player has also…

Understanding Which Mistakes Cost You the Most Money

I am fortunate enough to have worked for many years with the mental game coach…

Overbetting The Flop in Cash Games

Although most commonly analyzed on turns and rivers, flop overbetting can be a devastating weapon…

Using New Skills at the Poker Table

How many times has it happened to you that you make a mistake only to…

Flatting Ace-X Hands Shortstacked

Playing out of position is tricky, but it’s an essential part of tournament play. With…

Playing Limped Pots as the BB in MTTs

Success as the BB in limped pots begins before the flop. The BB’s equilibrium strategy…

The Absurd Game Theory of Chopped Boards

A “chopped board” in poker is one where the community cards make up the best…

Playing Limped Pots as the SB in MTTs

MTT confrontations between the small blind and big blind force no-limit players into uncomfortable situations,…

The Art of Learning Poker

In his book The Art of Learning, chess and Push Hands champion Josh Waitzkin describes…

Is Donk Betting for Donkeys?

“Donk betting”, or betting from out of position into the player who was the aggressor…

Delayed C-Betting

This is a companion piece to Probe Betting. It stands on its own, but understanding…

Probe Betting

As far as rules of thumb go in poker, “check to the raiser” is a…

ICM and Blind Battles: The Big Blind

This is a companion piece to this article on the SB’s strategy for blind vs…

ICM and Blind Battles: The Small Blind

ICM incentivizes more conservative play, which means that at stages of the tournament where risk…

The Initial Bettor’s Advantage

The mathematics of poker holds a little-known secret: the first bettor enjoys better bluffing odds…

Mastering the Chiplead: The Scalpel and the Sledgehammer

When you have a lot of chips at a final table or in another situation…

Flop Heuristics: IP C-Betting in Cash Games

Our never-ending quest for money and fame leads us to the flop. We open the…

How ICM Impacts Restealing From The Blinds

When I first started working with preflop solves, one of the features I found most…

The ICM Benefits of Late Registration in Poker Tournaments

Why do so many professional poker players register late for tournaments when they clearly would…

Flop Heuristics: OOP C-Betting in MTTs

Playing against an in-position cold-caller is dramatically different–and dramatically more difficult–than playing against a caller…

Counterintuitive Calls

Solver outputs such as those provided by GTO Wizard are models of no-limit hold ‘em,…

How To Negotiate Final Table Deals

Most people’s first introduction to the Independent Chip Model (ICM) is not from studying bubble…

How Does ICM Impact PKO Strategy?

If you have read The Theory of Progressive Knockout Tournaments you already know why we…

Understanding Blockers in Poker

Often when looking through a solver’s meticulously crafted grid of deception, one of the following…

Flop Heuristics: IP Cold-Caller in MTTs

A Cold-call refers to the act of calling a preflop raise when you don’t close…

Flop Heuristics: IP C-Betting in MTTs

In the world of poker, the flop is a crucial stage of the game that…

Flop Heuristics for Defending the Blinds in MTTs

The field of Game Theoretically Optimal poker is extensive, and thus, to simplify our strategy,…

Multiway strategy in Progressive Knockout Tournaments

Progressive Knockout (PKO) tournaments are much more complex than traditional MTTs. The fact that players…

How To Calculate Raises In Poker

One of the most frequently asked questions in poker is how to calculate the size…

Principles of River Play

The river offers the least complicated strategy of any betting street. With no further cards…

Exploitative Dynamics

GTO solutions are designed to be unexploitable, performing reasonably well no matter how your opponents…

How ICM Impacts Postflop Strategy

Most players understand how the Independent Chip Model (ICM) in poker impacts their strategy preflop,…

10 Tips for Multiway Pots in Poker

While lots of work has been placed into research and explanation of heads-up pot strategy,…

What is the Bubble Factor in poker tournaments?

The Independent Chip Model (ICM) shows us the real money implications of tournament chip decisions.…

The Theory of Progressive Knockout Tournaments

In poker, a PKO (Progressive Knockout) tournament is a type of tournament where a portion…

How To Analyze Turn Textures In Poker

Master the art of turn analysis in poker. Understand how the turn card changes the…

Principles of Turn Strategy

Learn the principles of turn strategy in poker and discover what makes the turn unique.…

Poker Strategies: Tournaments vs. Cash Games

Tournament poker is not as different from cash game poker as people sometimes assume. Most…

How Solvers Work

A Game Theory Optimal solver is an algorithm that calculates the best possible poker strategy.…

The Most Powerful Play in Poker

The central strategic implication of stack depth is the question of how much equity a…

When does ICM become significant in MTTs?

The Independent Chip Model (ICM) was invented in 1987 by M. Malmuth and is one…

How to Study GTO Solutions

Tools like GTO Wizard and other solvers should not be used to memorize specific strategies.…

Principles of GTO

Game theory, or GTO (for Game Theoretically Optimal), is best understood not as a rigid…

Interpreting Equity Distributions

GTO Wizard’s range vs range equity distribution graphs are an excellent tool for visualizing which…

What is Leverage in poker?

Leverage refers to the risk of future betting. When you call a bet on the…

Reasons for value betting in poker

You’re probably accustomed to thinking of bets as either value or bluff. In this taxonomy,…

The Science of Poker Performance

Poker is a game of small edges and big swings. Every hand is an investment…

What is Valor in poker?

Can a poker hand be courageous? How does your ability to value bet future streets…

Pot Geometry

“Pot Geometry” refers to betting an equal fraction of the pot on each street, such…

A Beginner’s Guide to Poker Combinatorics

Combinatorics is a fancy term for evaluating the number of possible “combinations” (combos) of any…

Stack-to-pot ratio

Stack-to-pot ratio, or SPR, is a way of measuring how deep the effective stack is…

Equity Realization

In poker jargon, equity expresses how much of the pot a hand will win, on…

Variance and Bankroll Management

Variance and Bankroll Management. Vital Soft Skills for Every Poker Player.

How to Become a GTO Wizard

Welcome to the wonderful world of game theory optimal poker! This article will serve as…

The Three Laws of Indifference

Indifference in poker is one of the most misunderstood concepts. The word “indifference” means that…

Poker subsets and abstractions

An “abstraction” is a way to simplify the game of poker. This game is so…

Mathematical Misconceptions in Poker

Pot Odds and MDF are foundational mathematical formulas in poker.

How to solve toy games

Poker is a complicated game. It’s impossible to calculate GTO strategies on the fly. By…

The Value of Fold Equity – Experiment

The term “fold equity” is ambiguous in the poker community. Firstly, it’s an EV equation,…

MDF & Alpha

MDF & Alpha. Minimum Defense Frequency and Alpha are metrics on poker that determine how…

What are Pot Odds in poker?

Pot odds are a fundamental calculation in poker. In the simplest terms, pot odds tell…

Does your range affect your strategy?

Advanced players will often tell you that your range affects your strategy.

Visualizing implied odds

Implied odds are the value you expect to gain over and above your raw equity.…

ICM Basics

As a tournament player, you may have heard about the concept of “ICM”, but what…

What is Equity in Poker?

The term “Equity” is ubiquitous throughout poker theory. Equity refers to your chances of winning…

Range Morphology

“Morphology” is the study of form or structure. You’ve probably heard terms thrown around such…

What is Expected Value in Poker?

Expected value (EV) is the most fundamental metric in poker. Every decision you make is…

Why doesn’t my solution match GTO Wizard?

So, you’ve got your own solutions to some spot, compared it to GTO Wizard, and…

Understanding Nash Distance

Understanding Nash Distance. One of the most common questions when studying with solvers is “Why…

Combinatorics Poker Puzzle

Today we have a special puzzle for you that will test your intuition as a…

The 10 Most Important Concepts for New Poker Players

The 10 Most Important Concepts for New Poker Players. Fundamentals are one of the most…

What is GTO in Poker?

The meaning of GTO in poker is Game Theory Optimal. Game theory is a study…

What does GTO aim to achieve?

So what exactly is a GTO strategy? What makes it “unexploitable”? What does it try…